Twenty Years of Fintech: The Transformation, Challenges and Future

Over the past decade and a half, the financial technology, or “fintech,” industry has completely transformed the way that the world uses, spends, and invests in money. From the start of digital banking and digital wallets to the rapid expansion of blockchain and cryptocurrencies, fintech has brought a multitude of new opportunities to consumers and financial businesses alike. These opportunities were enticing, as fintech has since rapidly grown in use with over 3.5 billion users expected in 2024, and a market worth over $2.26 billion as of 2023. Now, let’s break down how fintech started, how it has developed, and where consumers can expect the industry to go.

The Want For Change

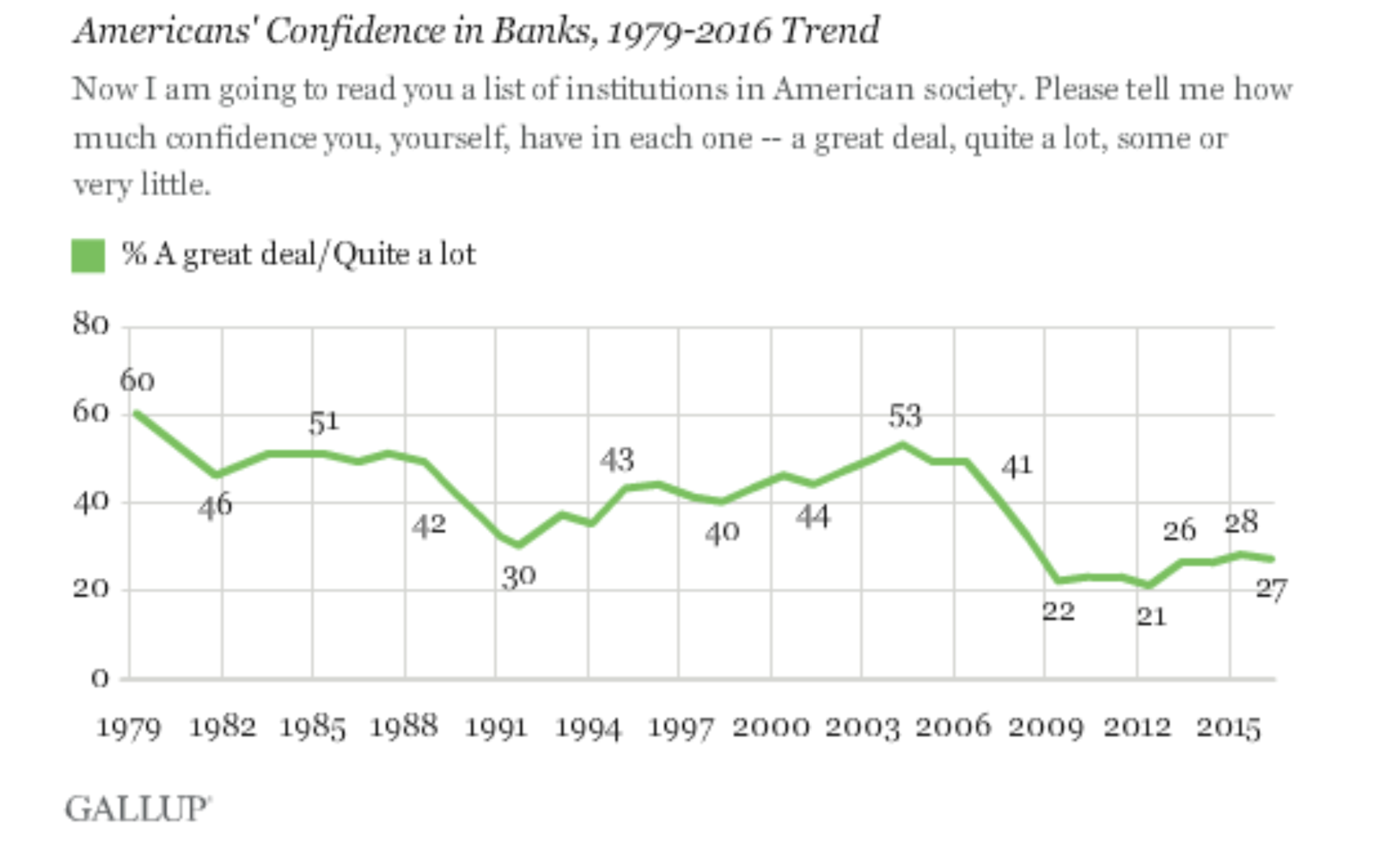

The rise of technology coupled with the financial recession of 2008 had a huge impact on the growth and development of fintech. Before 2008, there were some forms of digital banking, such as online banking platforms that allow users to check their accounts and conduct some forms of transactions. PayPal, one of the largest e-commerce companies, went public in February 2002 and allowed users to send money across borders and with expedited fund transfers. This was one of the first digital e-commerce spaces, but as smartphones continued to grow in popularity and technology continued to advance, fintechs began emerging more. After 2008, people were more distrustful of traditional banking and financial platforms and were more open to new solutions. Around the time of the recession, Americans’ confidence in traditional banking fell below 25 percent and remained there for years to follow. This made the attitude surrounding new banking options very positive, as Americans were open to a change in their financial ways.

Figure 1: Americans’ Confidence in Banks

The Bitcoin Boom

By 2009, with many Americans not feeling confident in their bank, a new financial option emerged; BitCoin. BitCoin was the first decentralized digital currency, which completely changed the way consumers could store and send finances. Cryptocurrencies, like Bitcoin, have allowed people worldwide to share and send money faster and easier than ever through a decentralized system. Cryptocurrency is digital money that does not require a financial institution to make purchases or complete transactions. Unlike traditional money, which requires a third-party financial institution to verify, crypto dollars are recorded on blockchain technology. Blockchain is decentralized, meaning the transactions do not have to go through a centralized platform, and in turn have more transparency and security per transaction due to the third-party platform being removed from the process. By leveraging the power of blockchain, transactions become not only more efficient but also universally accessible, making a significant change in how we conduct financial exchanges. As of March 2024, more than 46 million individuals have Bitcoin wallets with a minimum value of $1.

The Start of the Banking Transformation

As smartphones had quickly become a societal norm, finances, like everything else, needed to be easy to access, quick, and convenient for users. Users wanted to be able to see their financial accounts, make deposits, and send transactions all with one touch. Mobile-first banking had become more important and banks needed to keep up with the digitalization by offering new online mobile services, such as online bill pay and instant money transfers. In 2011, Google introduced the first digital wallet, which made it possible for users to pay via smartphone rather than using their card.

As mobile banking increased in popularity, embedded financial services also began coming to the forefront of the industry. Embedded finance involves integrating financial services into non-financial platforms, such as paying for your coffee through the Starbucks app that your debit card is linked to. Allowing non-banking entities to become involved in financial transactions transformed the traditional banking model. Another key transformation during this time was the introduction of buy now, pay later (BNPL) services. BNPL services are a form of short-term financing that allows consumers to make purchases and pay for them over time, typically without incurring interest if payments are made on time. This payment option has gained significant popularity, as it is often integrated into the checkout process of online retailers, making it easily accessible to consumers.

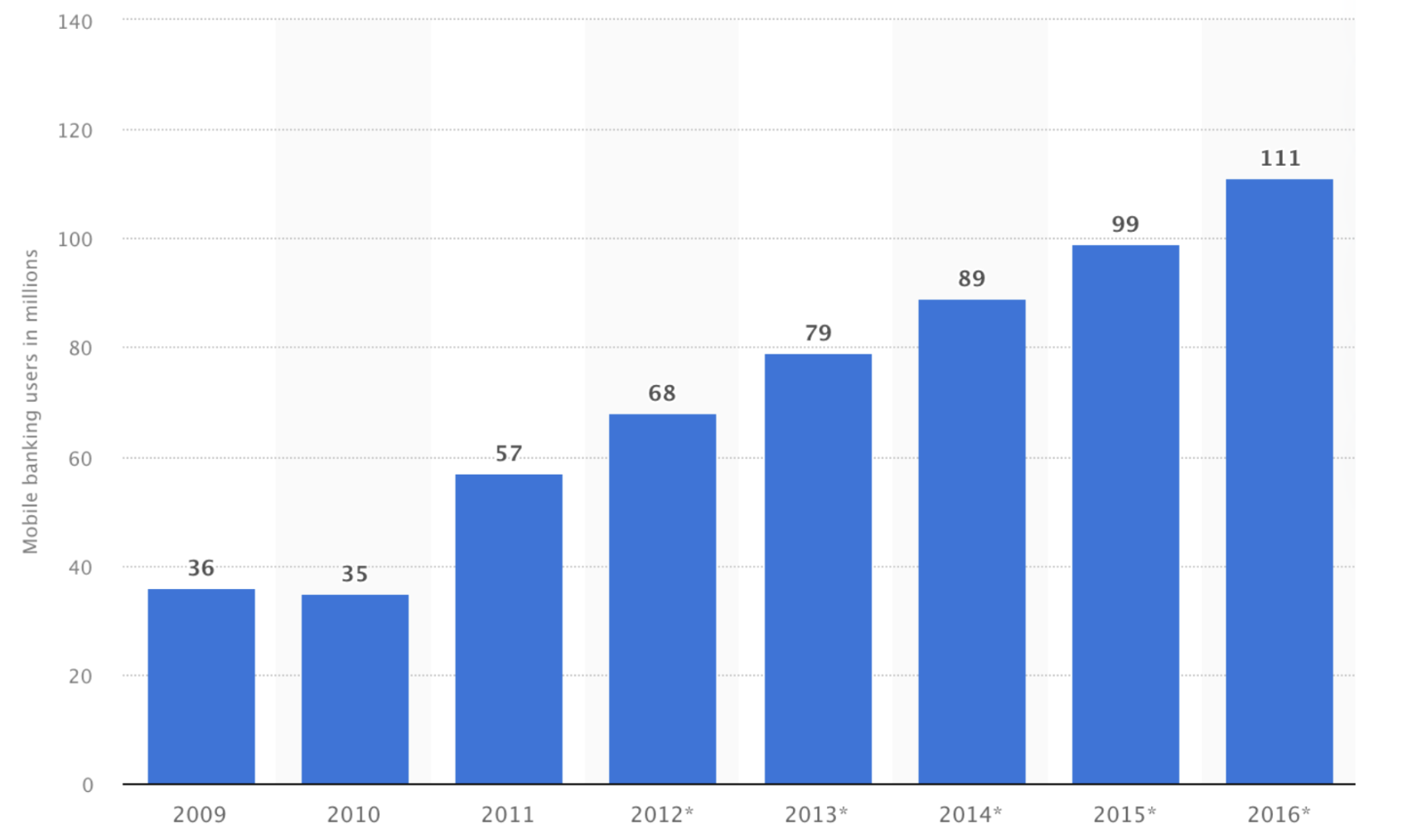

Figure 2: US Mobile Banking Users

By the mid-2010s, consumers were used to all aspects of finances being quick, easy, and convenient at their fingertips. Since Google’s digital wallet launch in 2011, US mobile banking had increased by over 30 thousand users by the time Apple Pay was released in late 2014. BNPL services like AfterPay and Klarna, were growing in use in the financial industry, and more people considered these services as financial tools. The mid-2010s were a period of financial exploration, digitalization, and inclusion, leaving consumers with more payment options than ever.

Say Goodbye to Physical Branches

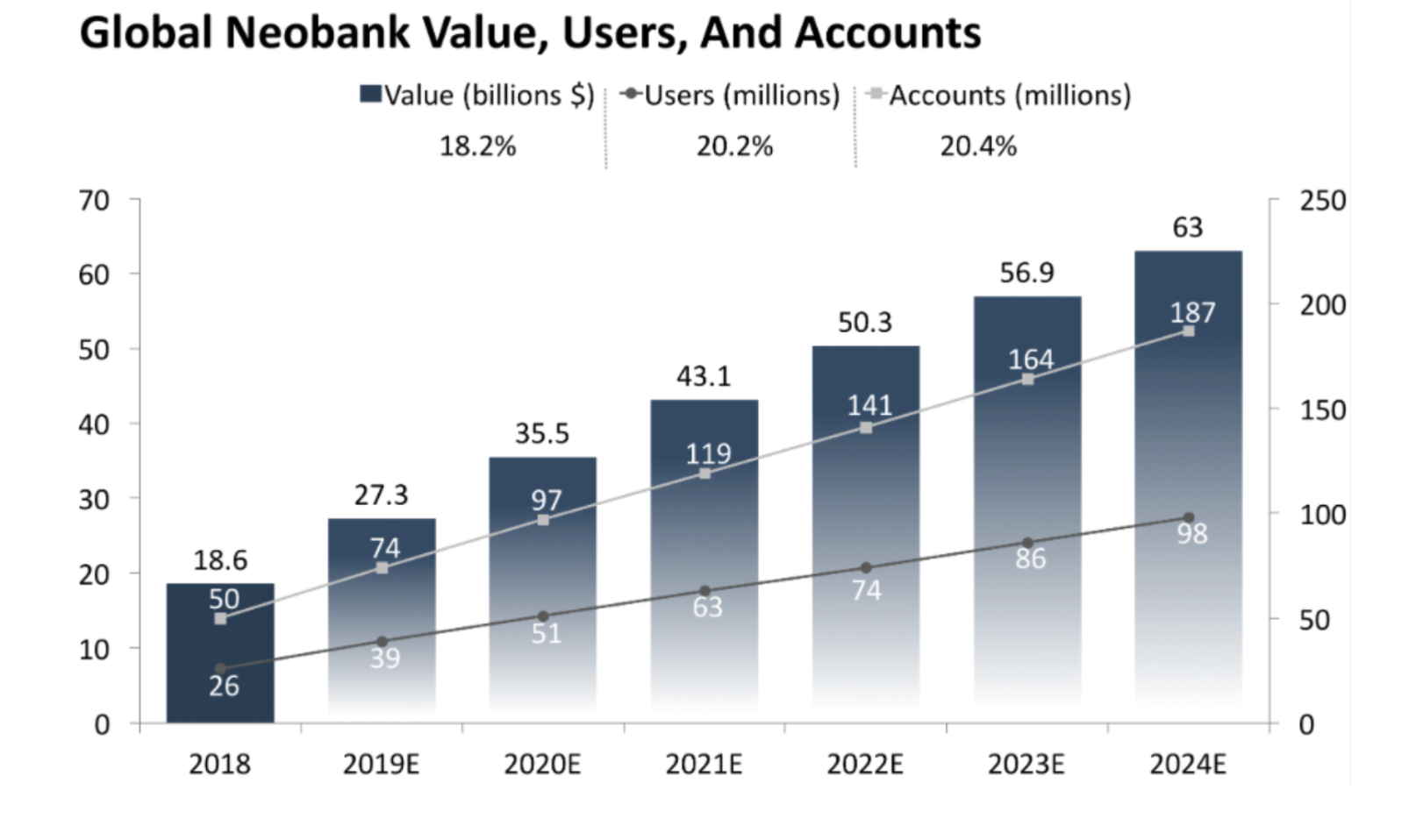

By the mid-2010s, some consumers were still being underserved financially, whether it be because they were facing too high fees or were simply lacking physical branches nearby. Following the massive amount of technological advancements and the rise of mobile banking, a new solution emerged; Neobanking. Neobanks are completely digital banks that prioritize financial inclusion by extending accessible services to underserved and unbanked populations and providing resources to enhance their financial well-being. Additionally, account opening could be effortlessly completed through a smartphone, which appealed to the newly digitally savvy customer base.

On the business side, neobanks were very appealing due to their low-cost structure. Their absence of physical branches, ATMs, or call centers resulted in a lean cost structure, which enabled neobanks to offer reduced fees and superior rates to traditional banks. With their agility and customer-centric approach, neobanks were well-positioned to capitalize on any gaps left by traditional banks in meeting evolving consumer needs. It became clear that the future of banking was going to be digital and mobile, and traditional banks needed to adapt to this new reality or risk being left behind in the digital revolution.

Figure 3: Global Neobank Growth

The Emergence of Artificial Intelligence

The next major transformation of the financial industry was the introduction of artificial intelligence (AI), and this was just the leverage that traditional banks needed to keep up. AI is software that mimics many of the functions humans can do, only at a much higher level and faster speed, which opened the door for more automated, optimized, and unique operation strategies. The first mainstream instances of AI are Apple’s Siri, which was launched in 2011, and Amazon’s Alexa, which was launched in 2014. As this software grew in popularity and the idea of AI became more accepted, financial institutions began to adapt it into their strategies in several key ways throughout the mid to late 2010s.

- Offering 24/7 Client Communication: Through the use of AI’s natural language processing, chatbox features offer customers in-depth and helpful responses to any questions they may have. Bank of America uses Erica as their AI virtual financial assistant, and there have been many satisfied customers with her personalized financial insight and advice.

- More Efficient Data Analysis: There is a massive amount of data being collected by financial institutions, but sorting through that data and analyzing it can be a lengthy and difficult process. AI can efficiently sort through data and provide useful insights at a much faster rate. Additionally, with the help of AI, things like fraud risk can be reduced by predictive analysis functions. Mastercard has recently implemented AI into their operations, through the use of Decision Intelligence, which is a fraud detection program. Similarly, American Express incorporated an AI fraud detection program to help better protect their credit card users. The speed and accuracy of AI detection have shown to be tremendously useful in reducing the risk of fraud and increasing the security of financial users.

- Better Personalization in Marketing: AI helps businesses segment their customers into more specific groups, so marketing can be more personalized and unique for what each customer group is looking for. For example, the things a recent college graduate is looking for from their bank are going to be very different from what a retired grandparent would be looking for. Artificial intelligence has tremendously increased the capabilities of hyper-targeting and allows marketers to create custom audience segments based on real-time data. Spatial.AI is a great example of the power of personalization that artificial intelligence provides. On this platform, public social media data is structured and organized into different audience segments. Marketers can see their most valuable audiences, while also learning about those audience’s online activity, lifestyle features, purchasing habits, and more. These audiences can be directly uploaded to your desired advertising platforms, ensuring that your catered message is targeted towards them.

Since its’ initial introduction, AI has become a driving force in the financial industry. 69 percent of banks are using AI to assist in their data analysis and customer service needs, and in the financial market, it is expected to reach over $26 billion by 2025. The benefits AI has brought to consumers and businesses alike are something that has revolutionized the expectations of the financial industry. Marketing can be more personalized and precise, consumers can receive help at any time of the day, and data is being analyzed faster than ever before.

COVID-19 As a Catalyst for Change

The COVID-19 pandemic significantly accelerated the growth and innovation within the fintech industry in the U.S. As traditional financial institutions faced operational challenges due to lockdowns and social distancing measures, many consumers and businesses turned to digital solutions for their financial needs. This shift not only highlighted the importance of fintech but also drove unprecedented adoption rates among users who may have previously been hesitant to embrace digital finance.

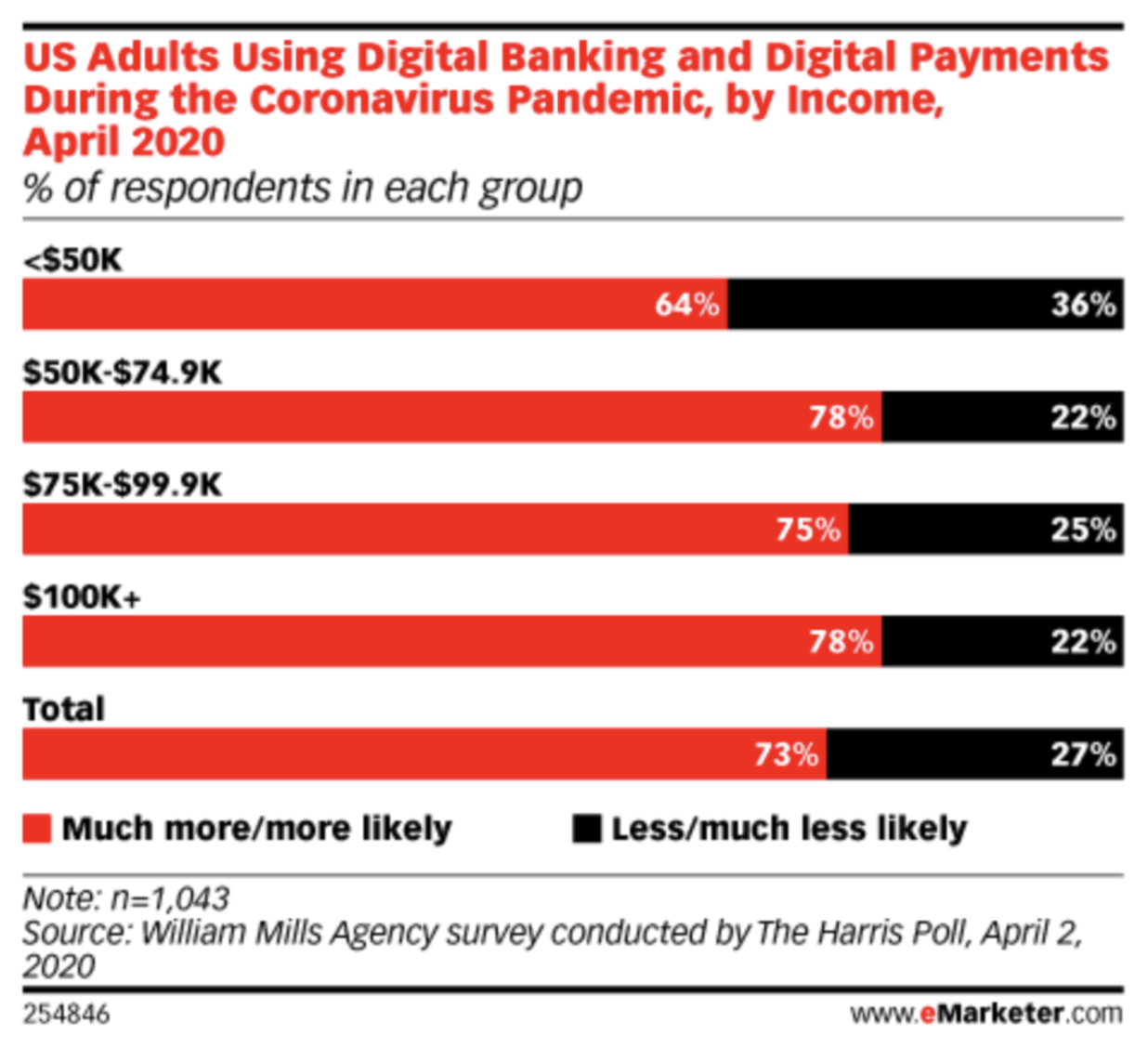

Figure 4: US Adults Using Digital Banking and Digital Payments

During the pandemic, fintech companies rapidly adapted their services to meet the evolving needs of consumers. For instance, many fintech lenders pivoted to offer new products aimed at supporting small businesses and individuals affected by the economic downturn. This included the introduction of recovery loan programs and enhanced digital banking services that required no physical contact. A big point of concern for many consumers centered around the closing of physical branch locations, and consumers who had not yet made the switch to digital banking were now turning toward it. 73 percent of Americans said they were more likely to turn to digital banking during the pandemic than before.

By 2020, digital finance had become an integral part of daily life for many Americans and the pandemic spurred a surge in the use of contactless payments, online banking, and mobile financial services. Although the crisis prompted fintechs to innovate quickly, it demonstrated resilience in the face of adversity and made many of these technologies more mainstream.

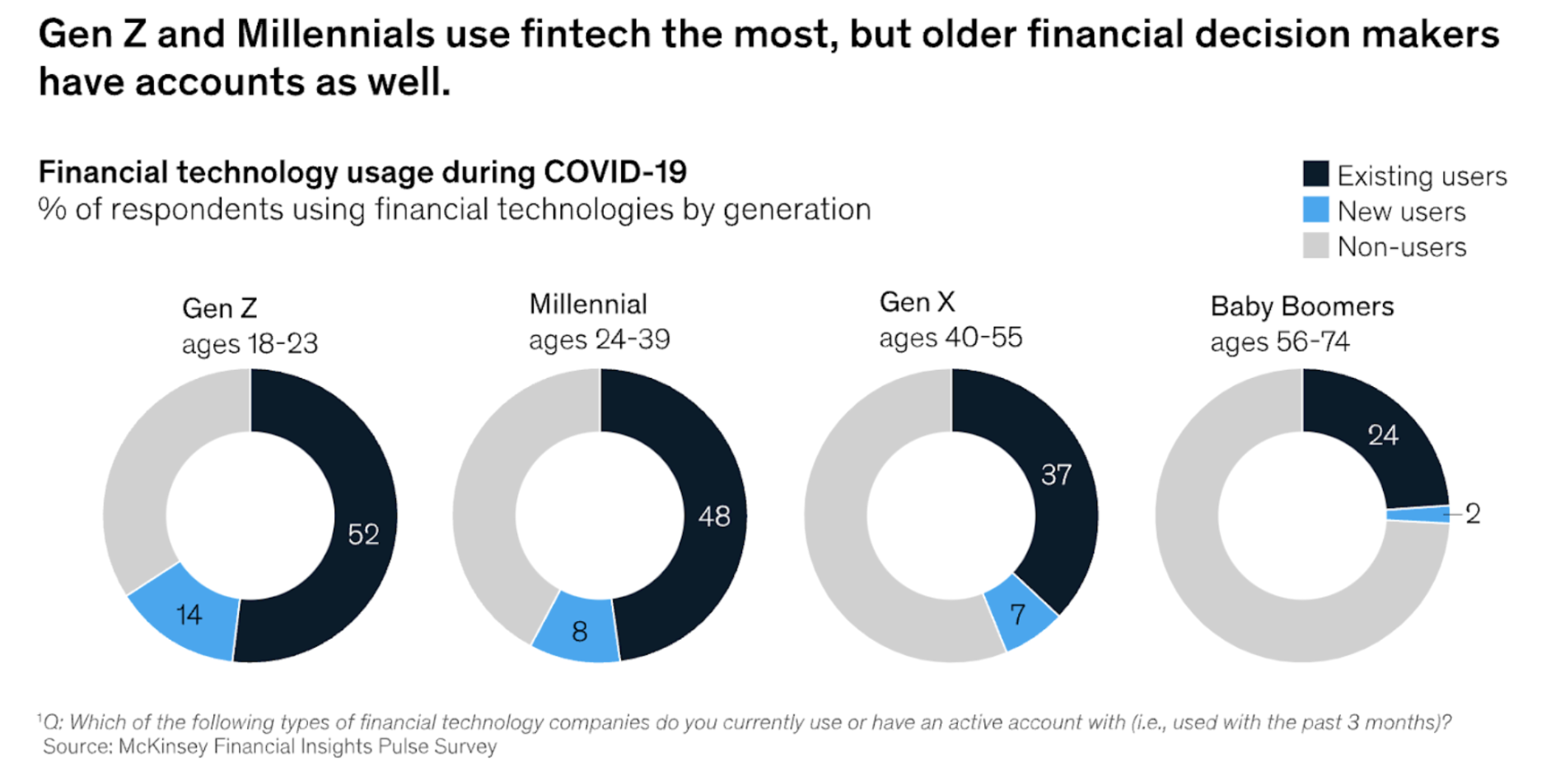

Figure 5: Financial Technology Usage During COVID-19

Emerging from the pandemic, the fintech sector is stronger and more competitive than ever. The increased reliance on digital solutions has led to a more robust financial ecosystem, with fintech firms continuing to innovate and expand their offerings. As the industry evolves, it is expected that technologies such as embedded finance and generative AI will further transform the landscape, creating new opportunities for both consumers and businesses.

Regulations and Concerns

Initially, there was not a lot of regulation surrounding fintechs, as the focus was more on market growth than risk management. However, as with the emergence of any new technology or financial platform comes a plethora of questions and concerns. How is customer data being used? How can neobanks and third-party platforms ensure the security of my transactions? People were becoming very concerned about things like fraud risk, money laundering, and ensuring the security of their financial information.

Cybersecurity has become a critical concern in the fintech landscape, as the rapid expansion into digital services exposes both companies and consumers to significant risks. Financial data breaches, identity theft, and transaction fraud are among the top threats that fintech firms face today. As these companies handle sensitive personal information, they must implement robust cybersecurity measures to protect against cyberattacks. This includes adopting comprehensive security frameworks, conducting regular risk assessments, and ensuring compliance with evolving regulations. By prioritizing cybersecurity, fintechs can not only safeguard their operations but also build trust with their customers, who are increasingly aware of the potential vulnerabilities associated with digital financial services.

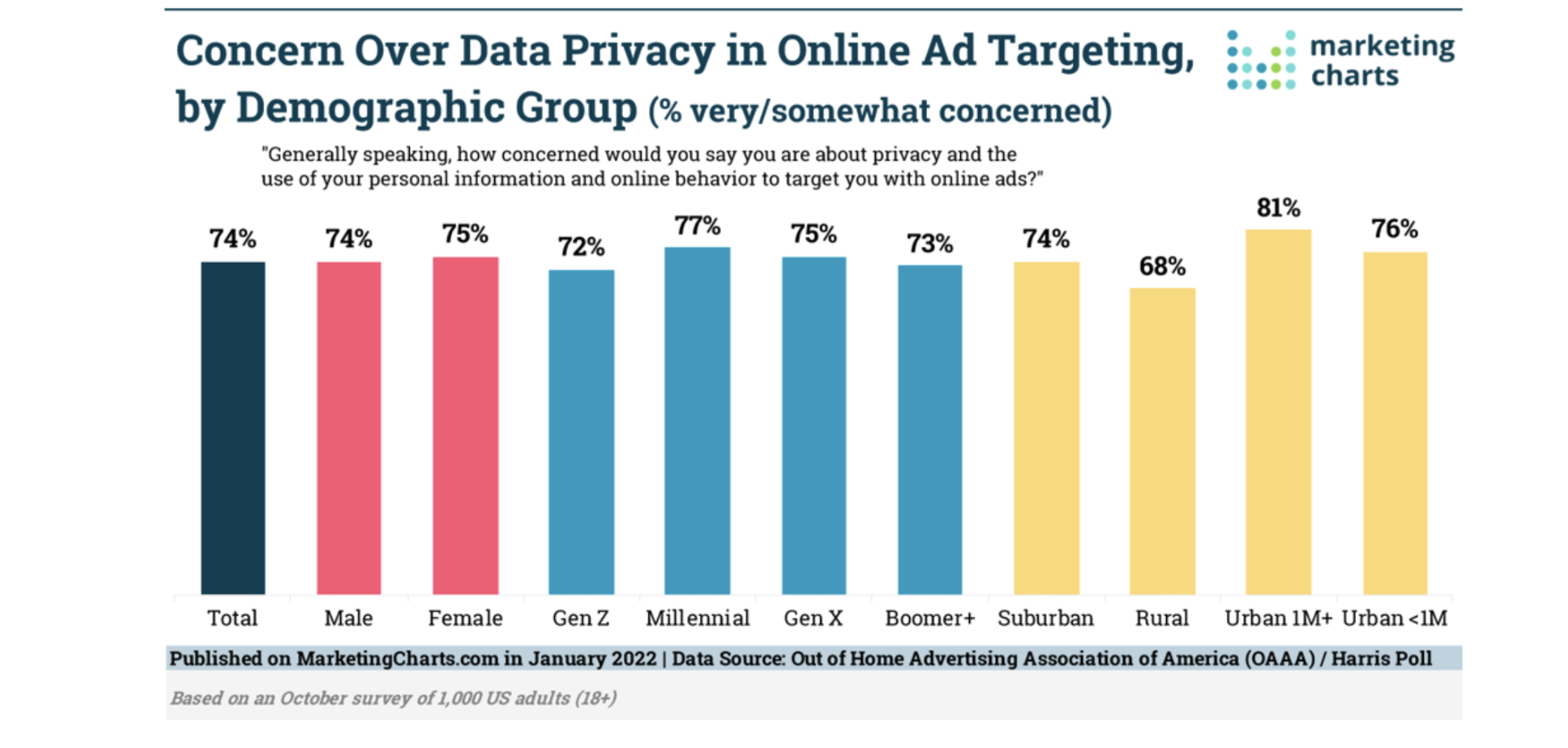

Starting with AI, there are several main concerns people have. Financial institutions will be responsible for storing very personal information, and consumers want to make sure they know how their data is being used. 68 percent of consumers worldwide are concerned about online data privacy, so businesses must be very explicit about getting consent to acquire data, what specific data will be used, and how the data will be used to better the customer’s overall experience. By ensuring your company has established a secure data governance plan, customers will feel more safe about providing their data.

Figure 6: Concern Over Data Privacy

Another issue with AI involves the inclusivity and bias recognition capabilities of the software. AI algorithms are trained using existing data sets, which sometimes contain certain biases or favor certain groups of people. For instance, if there is a bias in gender or race in the initial input data, the AI output will not be entirely objective. To prevent this from occurring, financial companies should continue to strive to have a diverse and multicultural human workforce, who can double-check the inputs for potential biases. Lastly, even though AI can do the job of a human through chat boxes and data assortment, 46 percent of bank customers still want a human connection as an option. Companies should work to find a balance between digital, or AI, interactions and human interactions to offer their customers the best experience. Additionally, with AI still growing and changing, having a real person monitor its tasks will decrease the likelihood of errors or mistakes occurring later down the road.

As the fintech industry evolves, challenging the traditional financial landscape, regulators must continuously adapt. There must be a balance between pushing innovation in fintech and ensuring the security of consumer’s finances and data information. With each new fintech advancement, it’s essential to develop regulatory approaches that ensure security and control while still promoting financial prosperity and inclusion.

What’s Next?

The fintech industry shows no signs of slowing down, with continuous advancements shaping the future of finance in ways that are both exciting and unpredictable. As we move forward, several key trends and developments are expected to further transform the landscape.

- Deeper Integration of AI and Machine Learning: The role of artificial intelligence (AI) and machine learning in fintech is set to expand even further. Financial institutions will likely continue to leverage AI for enhanced customer experiences, from ultra-personalized financial advice to predictive analytics that can anticipate customer needs before they even arise. Moreover, AI will increasingly be used to combat financial crimes, with more sophisticated fraud detection systems and real-time threat analysis, making transactions more secure than ever.

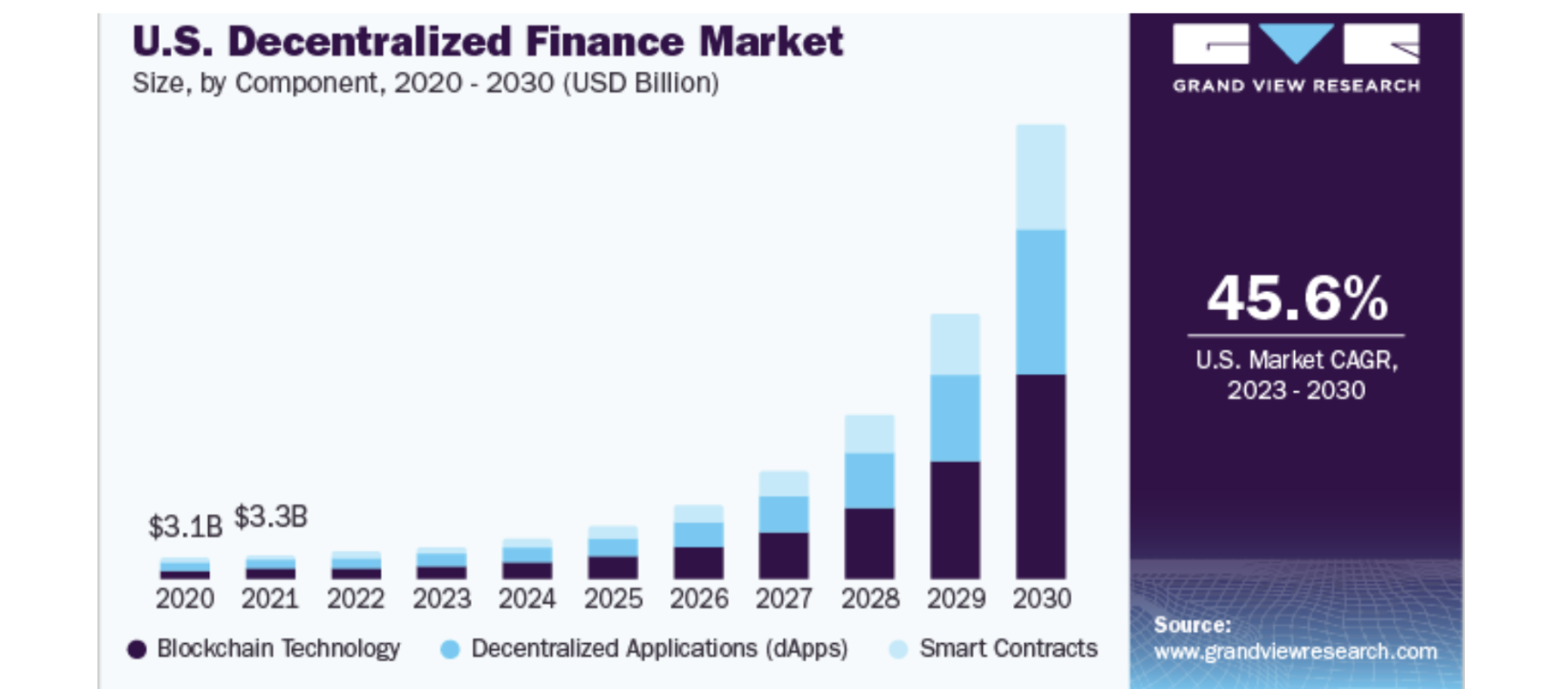

- The Growth of Decentralized Finance (DeFi): Decentralized finance, or DeFi, is poised to be one of the most revolutionary aspects of fintech in the coming years. By eliminating the need for traditional financial intermediaries, DeFi platforms allow for peer-to-peer financial transactions using blockchain technology. This shift could democratize finance, providing access to banking services for millions of unbanked individuals globally while offering more transparency and control to users. As DeFi continues to mature, we can expect it to challenge and perhaps even replace some conventional financial systems.

Figure 7: Growing DeFi Rates

- Expansion of Embedded Finance: Embedded finance is set to become even more ubiquitous as non-financial companies increasingly offer financial services directly within their platforms. This could include a more seamless integration of payment options, lending services, and even insurance products within everyday apps and websites. The convenience and accessibility of embedded finance are likely to drive its adoption, further blurring the lines between financial and non-financial industries.

- The Rise of Sustainable Fintech: As global awareness of companies’ environmental, social, and governance, or “ESG,” increases, the fintech industry is also likely to see a rise in sustainable and socially responsible financial products. This could include green banking initiatives, investment platforms focused on sustainable development goals (SDGs), and financial tools designed to promote ethical spending and investment. Fintech companies that prioritize sustainability and social impact will likely find themselves at the forefront of the next wave of industry growth.

- Continued Evolution of Digital Currencies: Digital currencies, including central bank digital currencies (CBDCs), are expected to become more prevalent as governments explore their potential benefits. These digital currencies could provide more efficient and secure transaction methods, reduce costs, and offer greater financial inclusion. As countries around the world experiment with CBDCs, the global financial system may undergo a significant transformation, with digital currencies playing a central role in everyday transactions.

The future of fintech promises to be dynamic and transformative. As technology continues to evolve, the industry will need to navigate new challenges and opportunities, ensuring that innovation benefits both consumers and businesses while maintaining security and trust. The next decade in fintech will likely bring even more profound changes, reshaping the way we manage, spend, and think about money.

For more financial tips and marketing strategies, check out our other articles here.

Like what you're reading?

Sign up for our Financial Experience Newsletter.